Do you get what you measure?

If only it were true. As every CEO knows all too well, very often you get much less than what you measure, and at worst, even something different.

Everything stems from a statement by a great English scientist, William Thompson or Lord Kelvin (1824-1907):

“When you can measure what you are talking about and express it in numbers, you know something about it. But when you cannot measure it, when you cannot express it in numbers, your knowledge is of a meager and unsatisfactory kind.”

The statement was later picked up and modified by W.E. Deming (1900-1993), the brilliant American engineer, essayist, teacher, and management consultant who taught the Japanese Total Quality Management. With which, incidentally, Japanese automotive companies ousted the U.S. auto industry from the market:

“The most important figures that one needs for management are unknown or unknowable, but successful management must nevertheless take account of them.”

On the other hand, the historian of control systems H.T. Johnson says:

“Perhaps what is measured is what will be achieved. More likely, what is measured is all that will be achieved. What is not measured (or cannot be measured) is lost.”

Following suit, the Israeli guru-entrepreneur E.M. Goldratt states:

“Tell me how you measure me, and I will tell you how I will behave. If you measure me in an illogical way, do not complain about illogical behavior.”

Since the topic is so crucial for Thauma, a clarification is in order.

The Goodhart’s Law

Charles Goodhart, a distinguished British economist and former professor at the London School of Economics, is the author of “Goodhart’s Law” which states that “any observed statistical regularity will tend to collapse once pressure is placed upon it for control purposes,” or that “when a measure becomes a target, it ceases to be a good measure.” The theme revolves around the possibility of unforeseen effects in the implementation of a program and is not new to economists.

In an imaginary nail factory, incentivizing workers to produce as many nails as possible, focusing on quantity rather than quality, could result in a mountain of tiny and useless nails. Conversely, incentivizing them based on the weight of the nails could lead to equally useless gigantic nails.

The German H. Siebert described, or rather invented from scratch, the “cobra effect”: he recounts that during the period of British rule in India, to address the problem of cobras infesting the city of Delhi, the authorities decided to offer a reward for every dead cobra delivered. Initially, it seemed to work, with a decrease in the presence of snakes. However, since feeding the snakes cost less than the reward offered, many started breeding them and then killing them to bring them to the authorities and pocket the bounty. When the authorities realized the unintended consequences of the program, they shut it down and stopped paying. At that point, since cobras were worthless, the breeders released all the snakes they were breeding, exacerbating the problem they initially sought to solve.

More generally, according to W. Wundt, we can talk about “unintended consequences” or “heterogenesis of ends”: “unintentional consequences of intentional actions” when a program triggers unforeseen outcomes, either for the better or the worse (almost always), due to aspects previously not taken into account.

Ultimately, just as with the “law of Goodhart,” the risk that the chosen measure is no longer an indicator, as it should be, but becomes an objective itself, overshadowing the real objectives, is high and increases with the complexity of the organization and the articulation of the interests and motivations of the individuals working in it. Given that it is impossible to completely avoid this difficulty, how can it be minimized?

How to Avoid the Consequences of Goodhart’s Law: The Company as a Whole

In the study of nature over the past two centuries, the natural sciences have achieved tremendous success by applying a “reductionist” approach: simplifying, biology is explained by the laws of chemistry, which in turn “reduces” to physics.

In organizations, to the extent possible, this method has also been applied: a strong division into increasingly specialized and narrow responsibility centers, analytical evaluation of individual performance, and a heavy use of psycho-social assumptions (sometimes only a priori and not verified a posteriori) about how individuals respond to incentives.

The great advantage of the “reductionist” approach is that it works because it reduces complexity. Analytical and industrial accounting is a way to divide the company into parts, each with its own management area for some item of the Income Statement.

So, a revenue center is responsible for sales in a certain product/market segment: it must sell the highest volumes possible at prices defined by marketing. A production cost center is responsible for efficiency in a certain phase of manufacturing. An expense center is responsible for the level of the various items it manages: personnel, services, etc.

The underlying idea of the control system based on economic responsibility centers is that at the lowest level of the organizational pyramid, elementary economic responsibility is assigned: those who purchase minimize purchase prices, those who produce maximize efficiency, those who sell maximize volumes.

Then, at the higher levels of the pyramid, someone with greater authority and responsibility synthesizes: they bring together revenues and costs and obtain a result, profit.

This image of the company as a well-functioning mechanical clock, as long as all the parts are well “oiled” according to the design, encounters its first practical limit when transitioning from Profit, Income Statement, to Invested Capital and Cash Flow (Balance Sheet and Statement of Cash Flows).

While it is relatively easy, at least in theory, though less so in practice, to divide the responsibility for profit into smaller elementary parts, when analyzing the formation of Invested Capital, the task becomes challenging in theory and almost impossible in practice.

The most important components of Invested Capital are three:

- Receivables from Customers

- Inventory (raw materials, work in progress, semi-finished goods, and finished products)

- Fixed Capital (real estate, plants, machinery, equipment).

Each component of Invested Capital is co-determined in its magnitude by many interdependent decisions made by various figures operating in the organization. The most significant case is that of inventory, where it can be said to be the “Murder on the Orient Express” because all travelers have given their stab to the victim.

Almost everyone in the company “works” to increase inventory and therefore invested capital, and no one is entirely responsible for its level and turnover:

- Purchasing gets better prices if they buy larger lots.

- Production increases efficiency if it manufactures more consistent batches.

- Sales are happier to have inventory to avoid missing opportunities.

- Design changes a component for technical reasons and creates slow turnover.

Organizations have developed many management tools to solve the problem. Among these, the most important is considering the company as a set of processes. Thauma indeed analyzes and expresses performance from this perspective.

But, above all, Thauma takes the CEO’s point of view, for whom the company is one entity, and everyone works for a single result.

How to avoid the consequences of Goodhart’s Law: the Balanced Scorecard

A very productive approach to reassembling performance at various levels of the organization into a unified synthesis, and thus aimed at overcoming Goodhart’s Law, is Thauma’s interpretation of the “Balanced Scorecard” (“BSC”). There’s much to say about the BSC (we’ve discussed it in this article), but at this moment, it’s important to illustrate the specific contribution of the BSC to overcoming, at least partially, Goodhart’s Law.

Firstly, the BSC manages to maintain a unified view of the company while reflecting its complexity. It does so by adopting an innovative perspective that surpasses both the purely process-oriented and the functional approach typical of “traditional” managerial accounting.

The BSC is precisely, as the name suggests, a way to assign a “balanced weight” to each performance that contributes to the overall company’s result.

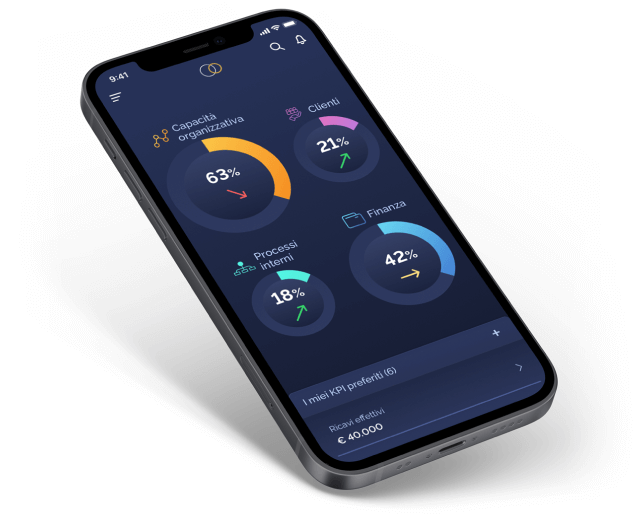

The BSC represents the company on 4 levels: at the base are the resources, which, for Thauma, are three (3 M):

- Materials

- Machines

- People (Man)

Thauma conventionally assigns an 11% weight to resources.

A “good” use, both effective and efficient, of resources produces efficient internal processes, which, in turn, generate effective customer service processes, leading to customer satisfaction. Thauma assigns a conventional weight of 11% to both the process and customer levels.

Efficient and effective processes yield good financial results. At this level, which is the most objective in a comparative logic among different organizations, Thauma assigns a weight of 67%.

In addition to the general BSC framework, Thauma identifies 3 fundamental performances that all businesses should pursue:

- Profit

- Cash

- Growth

In an objective comparison between different realities, the main weight is attributed to Profit (44%). Not because Thauma assumes that the company works for profit, but because profitability is the condition of the company’s existence.

And profit ensures, at least in the long term, the other two performances: self-financing (22%) and growth (34%).

While this is a summary description, it’s evident that Thauma overcomes the drawbacks described by Goodhart’s Law by articulating performances in a balanced manner, making it less susceptible to the unintended consequences of turning an indicator into a target.

It becomes almost impossible or significantly more challenging to:

- “Manipulate” the target.

- Sub-optimize the performances of the entire system due to the dominance of a single one.

Manipulating targets by those incentivized monetarily to achieve them is easier than it seems, unless those overseeing the process have a direct understanding of the work and context. This is the insurmountable limit of partial targets.

Those with greater ability to motivate choices, decisions, and results, those with informational asymmetries in their favor, are objectively able to manipulate both the goal-setting phase and the evaluation of their achievement (or non-achievement).

A skilled salesperson or a factory manager will always manage to “tilt” the assessment, both before and after the fact. Initiating a spiral of mutual “discounts” — “I ask for 100 because I know you’ll respond with 90,” to which the interlocutor replies, “I propose 80 knowing that you think I’ll propose 90” — is unproductive, costly, and dangerous.

Thauma’s choice, establishing objective weights, albeit conventional, is better than leaving the result to free negotiation between parties, where those with greater bargaining power prevail.

Thauma also counters the tendency for “particular” objectives, usually pursued by the stronger subjects in the organization, to prevail. The system is strongly based on a view of the company as a unique whole, built from interrelated parts, each with its role within the overall performance.

Thauma seeks and finds its effectiveness in adhering to a mode of thinking in harmony with that of SME CEOs: everyone’s salary comes from everyone’s work, and there’s only one pocket that pays for it.

This wisdom is supported by the sophisticated conclusions of a great control guru, R.N. Anthony (1916-2006), who states: “Although, for certain purposes, it may be useful to know all the manufacturing costs of a product, top management is absolutely unable to control a product and its production costs. What top management does, or at least tries to do, is to control the actions of the people responsible for these costs.”

From this perspective, the superiority of information such as Thauma’s emerges. It may be based on numbers that are perhaps less “precise” but are strongly correlated in their entirety with the performance objectives of the entire system. For the leaders of Italian companies, it serves as the true mirror reflecting their corporate reality.